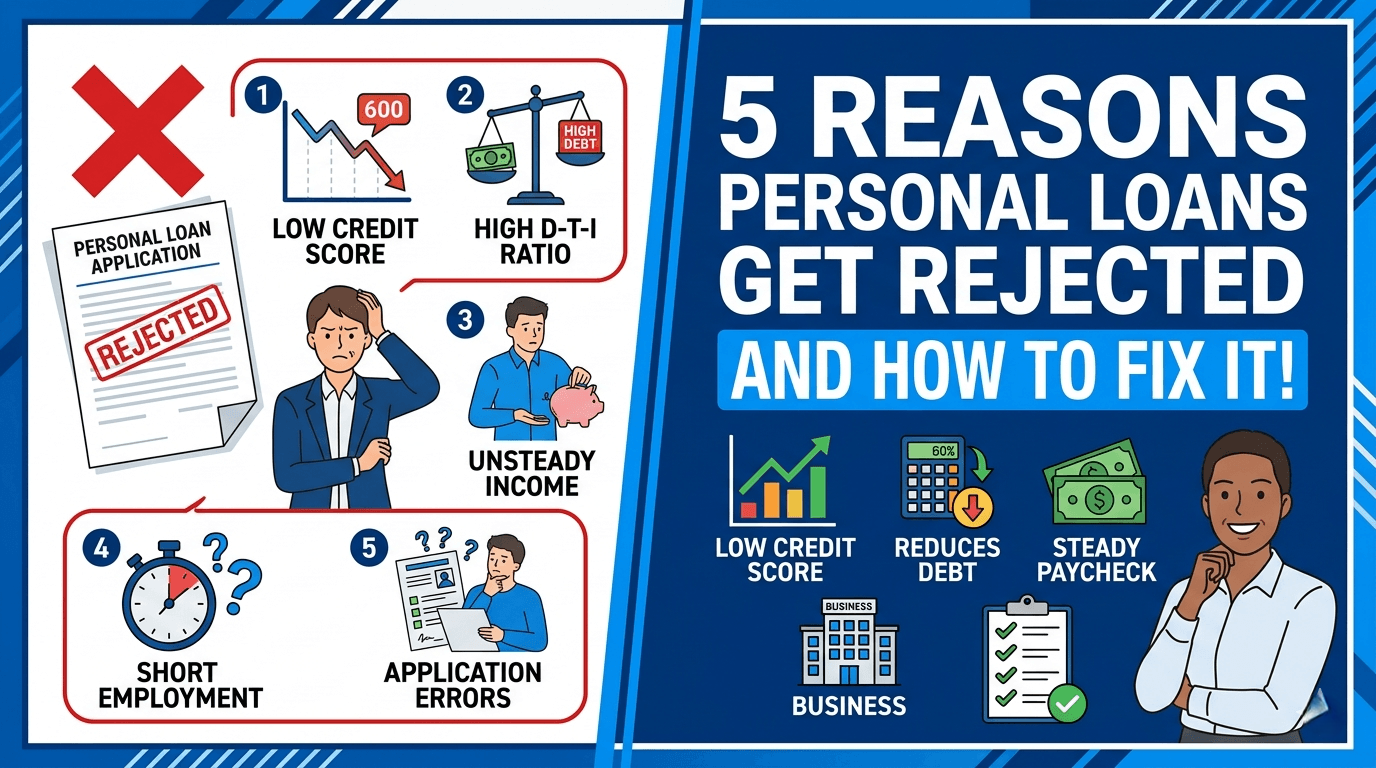

Quick Summary: 5 Reasons Personal Loans Get Rejected (And How to Fix It)

Half of all loan applications are rejected, but most are due to simple, fixable mistakes.

In 5 Reasons Personal Loans Get Rejected (And How to Fix It), we help you understand your right to know why a bank said no.

The best strategy? Identify the specific issue, fix it, and wait 3–6 months before reapplying to ensure your next application is successful.

What Banks Check Before They Say Yes

Banks look at four things in this order:

- Will you pay back? (Your credit score and payment history)

- Can you pay back? (Your income minus what you already owe)

- Are you stable? (How long you’ve had your job)

- Is your identity correct? (All documents matching)

Easy rule: If you fail #1 or #2, banks won’t even check #3 or #4. So fix your credit score or reduce your debt first.

The 5 Main Reasons for Rejection

1. Your Credit Score Is Too Low

What banks want: Most banks want a CIBIL score of 700 or higher.

What happens if lower: Below 650, rejection rates go above 60%. Below 600, almost no bank will approve you.

Why does this matter?

Your credit score shows if you’ve paid past loans on time. A low score tells the bank: “This person might not pay us back.”

How to fix it (3 steps):

- Step 1: Check your credit report for mistakes. 1 in 4 reports has an error.

- Step 2: Dispute any wrong information. This takes about 45 days.

- Step 3: Pay down your credit card balance to below 30% of your limit.

Expert quote:

“In my 12 years as a loan officer, 40% of people with scores between 580 and 620 had at least one fixable error on their report. Fixing errors is the fastest way to approval.”

— Vikram Mehta, former credit manager at HDFC Bank

Easy example:

Rahul had a 620 score because of a late payment that wasn’t his fault. He disputed it. Within 45 days, his score went to 710. He got his loan approved the next month.

2. You Owe Too Much Compared to What You Earn

The simple math:

Banks add up all your monthly loan payments. Then they divide by your monthly income.

Example:

- You earn ₹50,000 per month

- You pay ₹25,000 in EMIs (car + credit card + old loan)

- Your ratio = 50%

What banks want: Below 40%. Above 50% = almost certain rejection.

How to fix it:

- Pay off your smallest loan first

- Add a co-applicant (spouse or parent with income)

- Wait until one loan ends before applying for a new one

Easy example:

Sunita earned ₹48,000 and paid ₹25,000 in EMIs (52% ratio). She got rejected. She used her bonus to pay off a small loan. Her EMI dropped to ₹18,000 (37% ratio). She reapplied and got approved in one week.

Extra tip: Some banks add living expenses to your debt. Ask the loan officer which formula they use.

3. You Haven’t Had Your Job Long Enough

What banks want (salaried people):

- At least 12 months of total work experience

- At least 6 months in your current job

What banks want (self-employed):

- 3 years of tax returns

- Steady or growing income

Red flags banks notice:

- You’re still on probation

- You’ve had 3+ jobs in 2 years

- Gaps in employment longer than 3 months

- Freelance income that goes up and down a lot

How to fix it:

- Don’t apply during probation – wait for your confirmation letter

- If self-employed, pay yourself a monthly “salary” from your business

- Keep business and personal bank accounts separate

Easy example:

Anjali started a new job 2 months ago. She applied for a loan during probation. Rejected. She waited 4 months until her confirmation letter came. Then she reapplied and was approved.

Expert quote:

“Self-employed people get rejected 35% more often than salaried workers. The best thing you can do is show regular monthly income, even if it’s a small salary from your own company.”

— Priya Nair, small business lending specialist

4. You Applied to Too Many Banks Too Quickly

Here’s what happens:

Every time you apply to a bank, they check your credit. That’s called a “hard enquiry.” Each hard enquiry drops your score by 3–10 points.

But worse than the points drop? It makes you look desperate.

| Type of Check | Who Does It | Hurts Your Score? |

|---|---|---|

| You check your own score | You | No |

| Bank checks when you apply | Bank | Yes (3–10 points) |

The rule: Never apply to more than one bank in a 90-day window.

How to fix it:

- Use pre-approval tools (these are “soft checks” – they don’t hurt your score)

- Space out applications by at least 3 months

- Don’t believe the “14-day shopping window” myth – that’s only for home loans

Easy example:

Priya applied to 4 different lenders in 10 days. Her score dropped from 745 to 698. All 4 rejected her. She waited 4 months without applying anywhere. Her score went back to 722. Her 5th application was approved.

5. Your Documents Don’t Match

The most frustrating rejection – but also the easiest to fix

Up to 15% of rejections happen because of document mistakes, not credit problems.

Common mistakes:

- Your PAN card says “R. Sharma” but your Aadhaar says “Rajesh Sharma”

- The date of birth is different on two documents

- You said you earn ₹50,000 but your bank statement shows ₹40,000

- Your address proof expired 2 months ago

- You forgot to sign the form

How to fix it:

- Use the EXACT same name on every document

- Check your income number against your payslip THREE times

- Make a checklist before submitting

- Ask the bank officer to check your documents BEFORE they do a hard credit check

Easy example:

Ravi’s PAN said “Ravi K” but his Aadhaar said “Ravi Kumar.” The bank rejected him without even checking his credit score. He corrected his Aadhaar to match his PAN. He reapplied with the same documents. Approved in 3 days.

2 Hidden Reasons (Most Articles Don’t Tell You)

Hidden Reason #1: You Have No Credit History (Thin File)

This happens if you’ve never taken a loan or credit card. Banks don’t know if you’re trustworthy because they have no record of you.

The fix: Get a “secured” credit card (you deposit ₹10,000–₹25,000 as security). Use it for 6 months. Pay on time. You’ll build a good score without taking on real debt.

Hidden Reason #2: The Bank Already Gave You Too Much

Some banks have internal limits. If you already have a home loan and car loan from the same bank, they might say no to a personal loan – even if your numbers look fine.

The fix: Apply to a different bank where you have no existing loans. Don’t tell them you want “all loans in one place” – that makes them nervous.

What to Do in the First 24 Hours After Rejection

- Ask why – Banks must tell you the reason (it’s the law in many countries and RBI guideline in India)

- Check your credit report within 7 days

- Fix the specific problem (score, debt, documents, or job history)

- Wait 3 months – DO NOT apply again immediately

- Apply to only ONE bank when you try again

- Use a soft-check tool first to see if you’ll get approved

- If rejected again, try a secured loan or add a co-signer

Where to Apply If Normal Banks Say No

| Type of Lender | Ease of Approval | Interest Rate | Best If… |

|---|---|---|---|

| Government Banks | Very Hard | 10–14% | Your score is 750+ |

| Private Banks | Hard | 12–18% | Your score is 700+ |

| NBFCs | Medium | 14–22% | Your score is 650+ |

| App-based Lenders | Easy | 18–30% | Score 600+ or no history |

| Credit Unions | Medium | 10–16% | Member with steady income |

Frequently Asked Questions (12 Questions)

1. Can I get a loan with a 600 credit score?

Yes, but only from app-based lenders. Interest will be high (18–30%). Better to wait 3–6 months and improve your score first.

2. How long should I wait after rejection?

At least 3 months. 6 months is better if you’re fixing credit problems.

3. Does checking my own score lower it?

No. Never. You can check your score every day if you want.

4. Will adding a family member help?

Yes, if they have good credit and steady income. But they become responsible for the loan if you can’t pay.

5. Can I appeal a rejection?

Yes. Ask for the reason in writing. If it’s a document mistake, you can sometimes fix it and reapply immediately.

6. Do all banks use the same rules?

No. Government banks are strictest but have lowest rates. App-based lenders are easiest but expensive.

7. Does rejection hurt my credit score?

No. The hard check done BEFORE the rejection hurts your score. The rejection letter itself does nothing.

8. Can I apply to two banks at the same time?

Don’t. Each one does a hard check. Each hard check lowers your score. Space them out by 3 months.

9. Should I close old credit cards before applying?

No. Keeping old cards open helps your credit history length. Just don’t carry a balance.

10. Can I get a loan during my probation period?

Almost never. Wait until you get your confirmation letter.

11. What’s the minimum income to get a loan?

Most banks want ₹25,000+ per month. Some app-based lenders go as low as ₹18,000.

12. Will a loan rejection affect my job search?

No. Employers don’t see your loan rejections. Only serious legal problems (bankruptcy, court judgments) show up.

The Bottom Line

Getting rejected feels bad. But most rejections are fixable.

Do this: Check your credit report. Lower your existing debt. Wait 3 months. Apply to only one bank.

Don’t do this: Apply to five banks in one week. Ignore document errors. Reapply immediately.

Fix the real problem first. Then try again. You’ll get approved.

1 thought on “5 Reasons Personal Loans Get Rejected (And How to Fix It)”