A Simple Guide for Indian Borrowers

You need a loan. You see three options: a bank, an NBFC, or an online lender app. Which one is right for you? Also, make sure to review the complete checklist of documents for loan approval before applying.

The answer depends on three major things:

- Your CIBIL score

- How fast you need the money

- How much you want to pay in interest

This guide explains the differences in simple language. No jargon. No complicated tables. Just clear advice.

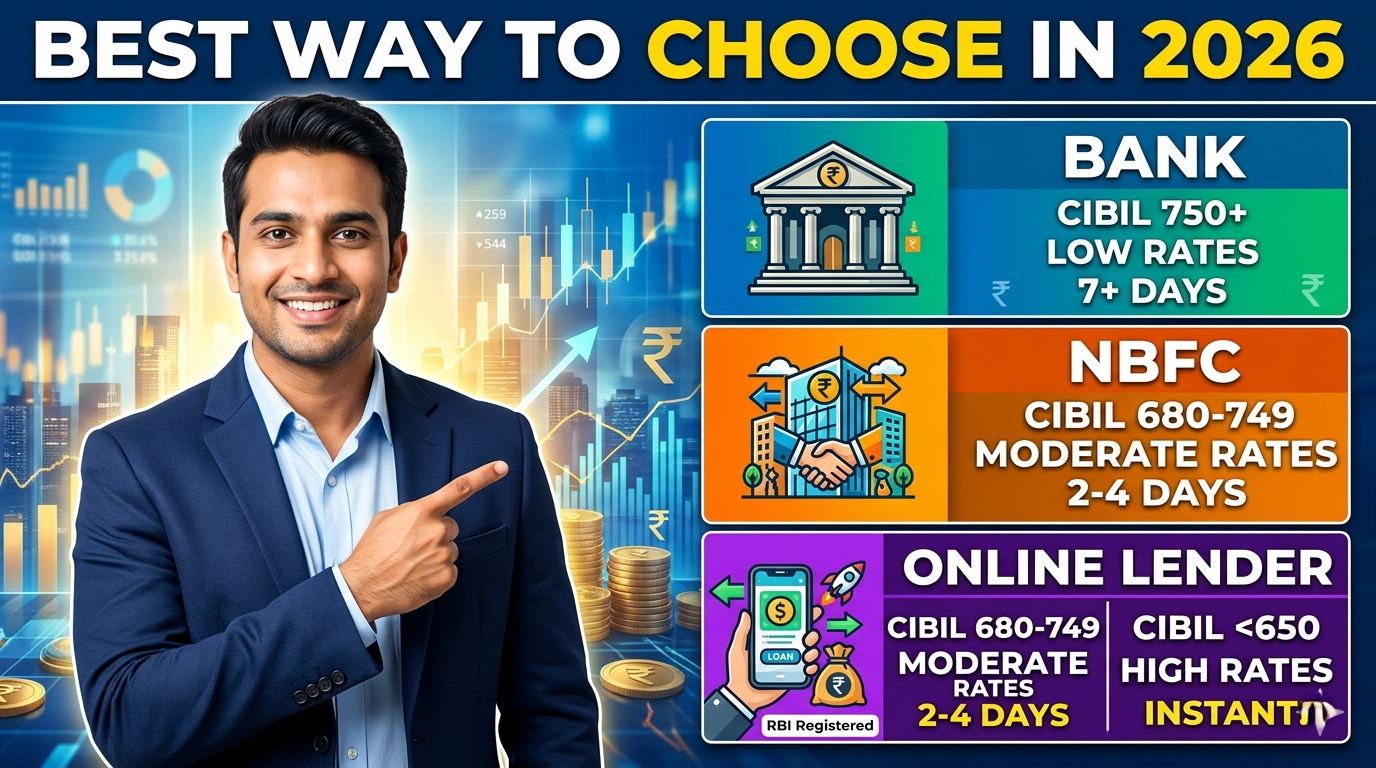

Bank vs NBFC vs Online Lender: Best Ways to Choose

Now let us understand each option in detail.

What Is a Bank?

A bank is a place that takes money from people as deposits and gives loans to others. Examples are SBI, HDFC, ICICI, and Bank of Baroda. Banks are controlled by the Reserve Bank of India (RBI). They follow strict rules.

How much do banks charge?

Interest rates for personal loans are between 9% and 15% per year.

How long does a bank take?

Between 3 and 15 days. Sometimes longer.

What CIBIL score do you need?

750 or above. Banks are strict about this.

A real example:

A government employee with a CIBIL score of 810 applied for a ₹10 lakh loan for home renovation through SBI. Within 5 working days, the loan was approved at 9.8% interest. The processing fee was just ₹2,500. The bank also allowed a 3-month break before EMIs started.

Another example:

A salaried employee with a CIBIL score of 782 applied for a ₹5 lakh loan. A public sector bank gave him 10.25% interest. The processing fee was 0.85%. He got the money in 9 days.

When should you choose a bank?

Choose a bank when you are planning a big expense like home renovation, wedding, or children’s education. Banks give the lowest interest rates. But you must be patient.

What Is an NBFC?

NBFC stands for Non-Banking Financial Company. These are companies that give loans but do not take deposits from the public like banks. Examples are Bajaj Finance, Tata Capital, L&T Finance, and Mahindra Finance. They are also registered with the RBI.

How much do NBFCs charge?

Interest rates for personal loans are between 11% and 18% per year.

How long does an NBFC take?

Between 2 and 7 days. Faster than banks.

What CIBIL score do you need?

700 or above. Some NBFCs accept 680 if you have a good income.

A real example:

A small business owner with a CIBIL score of 715 applied for a ₹3 lakh business loan through an NBFC. The loan was approved in 4 days at 14.5% interest. The processing fee was 2%. Unlike a bank, this NBFC also offered an overdraft facility. That means he could withdraw money as needed, up to 80% of the loan limit.

When should you choose an NBFC?

Choose an NBFC when your CIBIL is good but not excellent. Also choose an NBFC if you are self-employed or run a small business. NBFCs are more flexible than banks.

What Is an Online Lender?

Online lenders are companies that give loans through mobile apps. Examples are CASHe, EarlySalary, MoneyView, and KreditBee. Some online lenders are actual NBFCs with their own license. Others are just technology companies that connect you to a bank.

Important warning:

Only use online lenders that are registered with the RBI. The RBI will publish a public list of approved digital lending apps starting June 15, 2025. If an app is not on that list, do not use it.

How much do online lenders charge?

Interest rates are between 14% and 29% per year. This is much higher than banks and NBFCs.

How long does an online lender take?

Between 15 minutes and 24 hours. Very fast.

What CIBIL score do you need?

As low as 550. Online lenders use alternative data like your UPI payment history, rent payments, and mobile phone bills.

A real example:

A freelance designer with a CIBIL score of 620 needed ₹40,000 to buy equipment for a new project. An RBI-registered online lender approved the loan within 3 hours. The interest rate was 22%. The processing fee was 4%. The total cost over 12 months was ₹50,400. She paid ₹10,400 extra for the speed and convenience.

When should you choose an online lender?

Only in emergencies. For example, a medical emergency or urgent travel. Do not use online lenders for planned expenses. The interest is too high.

What Is a Key Fact Statement (KFS) and Why Does It Matter?

A Key Fact Statement (KFS) is a simple one-page document that every lender must give you before you sign the loan agreement. It shows:

- The interest rate

- The processing fee

- All other charges

- The total cost of the loan (called APR)

- Your monthly payment amount

- The penalty for late payment

- The penalty for paying early

Important rule from RBI (2025):

The KFS must be valid for at least 3 days. This means you have 3 days to read it, compare it with other lenders, and decide. If a lender asks you to sign within minutes, they are breaking the law. Walk away.

Comparison Table – Banks vs NBFCs vs Online Lenders

At-a-Glance Comparison

Evaluate lenders side-by-side using key performance and regulatory criteria.

| Feature | Banks | NBFCs | Online Lenders (RBI-reg.) |

|---|---|---|---|

| Interest rate | 9 – 15% | 11 – 18% | 14 – 29% |

| Processing fee | 0.5 – 2% | 1 – 3% | 2 – 6% |

| Loan approval time | 3 – 15 days | 2 – 7 days | 15 min to 24 hours |

| Minimum CIBIL needed | 750+ | 680 – 700+ | 550+ |

| Gives a Key Fact Statement? | Yes | Yes | Yes |

| 3 days to review KFS? | No | Yes | Yes |

| Reports to CIBIL? | Yes | Yes | Most do (84%) |

| Best for… | Planned big expenses | Self-employed, small business | Emergencies, low CIBIL |

Hidden Fees You Must Know About

Many borrowers only look at the interest rate. That is a mistake. You must also look at three other costs.

First, processing fee and GST.

Every lender charges a fee to process your loan. This is 0.5% to 6% of the loan amount. Then you pay 18% GST on top of that fee.

Example for a ₹1 lakh loan:

- Bank (1% fee): ₹1,000 fee + ₹180 GST = ₹1,180 total

- NBFC (2% fee): ₹2,000 fee + ₹360 GST = ₹2,360 total

- Online lender (4% fee): ₹4,000 fee + ₹720 GST = ₹4,720 total

Second, late payment penalty.

If you miss an EMI, you pay a penalty. Banks charge around ₹500 plus GST. NBFCs charge around ₹750 plus GST. Online lenders charge around ₹800 plus GST plus daily interest.

Third, prepayment penalty.

If you want to pay back the loan early, some lenders charge a penalty. Banks usually charge 2-3% if you pay early within the first 12 months. NBFCs charge 3-5%. Some online lenders charge 0% after 3-6 months. Always check the KFS for this.

Red flag warning:

If a lender asks you to pay a “processing fee” before they give you the loan, stop immediately. That is illegal. Legitimate lenders deduct the fee from the loan amount or ask you to pay after disbursal, never before.

Safety Checklist – 6 Steps Before You Apply

Use this checklist for every loan application.

Step 1: Verify RBI registration.

Go to the RBI website (rbi.org.in). Search for the lender’s name in the NBFC list. If you cannot find them, do not apply.

Step 2: Ask for the Key Fact Statement.

If the lender refuses or delays, stop the application. A legitimate lender will give you the KFS immediately.

Step 3: Check the 3-day validity period.

The KFS must say that the offer is valid for at least 72 hours. If it says 24 hours or less, the lender is violating RBI rules.

Step 4: Confirm how you will receive the money.

The full loan amount must go directly from the lender’s bank account to your bank account. No third party. No deduction before transfer.

Step 5: Find a physical address.

The lender must have a real office address on their website. A Gmail address and a WhatsApp number are not enough. Those are signs of a fake lender.

Step 6: Look for the NBFC registration number.

This is a 14-digit number on the lender’s website. It should start with “05” or “13”. If it is missing or looks fake, do not proceed.

A real warning:

Google removed over 4,700 illegal loan apps between 2023 and 2025. Just because an app is on the Play Store does not mean it is safe. Always verify with the RBI.

Which One Should You Choose? A Simple Decision Guide

Choose a bank if:

- Your CIBIL score is 750 or higher

- You need more than ₹2 lakh

- You can wait 7 days or more

- You want the lowest possible interest rate

Choose an NBFC if:

- Your CIBIL score is between 680 and 749

- You need between ₹1 lakh and ₹3 lakh

- You can wait 2 to 4 days

- You are self-employed or have a small business

Choose an RBI-registered online lender if:

- Your CIBIL score is below 650

- You need less than ₹1 lakh

- You need the money within 24 hours

- You have an emergency and no other option

Frequently Asked Questions (12 Questions)

1. Which lender has the lowest interest rate?

Banks. They charge 9% to 15%. But you need a high CIBIL score above 750.

2. Can I get a loan with a CIBIL score of 550?

Yes. Some RBI-registered online lenders will approve you. But the interest rate will be very high, between 24% and 29%.

3. Are NBFCs safer than online lenders?

All RBI-registered NBFCs are safe. Online lenders are safe only if they are on the RBI’s approved list. Unregistered apps are never safe.

4. Which lender is the fastest?

Online lenders. They can approve and send money within 15 minutes to 3 hours.

5. Do online lenders report to CIBIL?

About 84% of registered online lenders do. Always ask before you sign: “Do you report my payments to CIBIL?” If they say no, your on-time payments will not improve your credit score.

6. What is a Key Fact Statement?

A one-page document that shows the complete cost of your loan. It is required by RBI law. Do not sign any loan without reading it.

7. Can I repay an online loan early without penalty?

Some online lenders allow this after 3 to 6 months. Check your KFS. If the KFS does not mention early repayment, assume there is a penalty of up to 6%.

8. How do I spot a fake online lender?

Look for these signs: they ask for money before giving the loan, they have no physical address, they refuse to give a KFS, they pressure you to sign within minutes, or they want to send money to a third-party account.

9. Which lender is best for a business loan without collateral?

NBFCs like Bajaj Finance and Tata Capital. Banks usually want collateral for business loans above ₹10 lakh.

10. Can I build my CIBIL score using an online lender?

Yes. Take a small loan from an RBI-registered online lender. Repay it on time. After 6 to 12 months, your CIBIL score will improve. Then you can apply for a cheaper bank loan.

11. What if I already signed a loan without a KFS?

You have less legal protection. The KFS is the only document the RBI recognises as proof of disclosed costs. For future loans, always demand the KFS before signing.

12. Do the new RBI rules apply to old loans taken before 2025?

No. The new rules apply only to loans sanctioned after June 2025. But if your lender offers you a “top-up” or renewal after that date, the new rules apply to that new portion.

Final Advice

Choosing the right lender is not complicated. Follow this simple rule:

Bank for low cost. NBFC for balance. Online lender only for emergencies.

Before you sign anything, get the Key Fact Statement. Read it carefully. Check the 72-hour validity. Verify the lender on the RBI website.

A legitimate lender will answer all your questions patiently. A fake lender will rush you and hide information.

Your signature is powerful. Use it wisely.