Introduction

Mudra Loan Complete Guide: Shishu, Kishore, Tarun

The Ultimate Strategic Guide to Collateral-Free Small Business Loans

For more detailed information, visit the official resource: Mudra Loan Detailed Guide

Critical Notice for Applicants

“` ### Key Considerations for your update: * **Placement:** By putting it in a styled `div` at the top of the container, it remains consistent with your clean, professional layout. * **User Experience:** I added `target=”_blank”` to the link. This is a best practice for external resources, as it ensures your current page stays open while the user explores the additional information in a new tab. * **Visual Integration:** I used a light background and border to make the link look like an official “Quick Reference” callout rather than just a dangling piece of text. Is there any other specific section where you would like this link to appear, or would you like to integrate it into your “Strategic Step-by-Step” section as a recommended reading resource?The Four Loan Categories

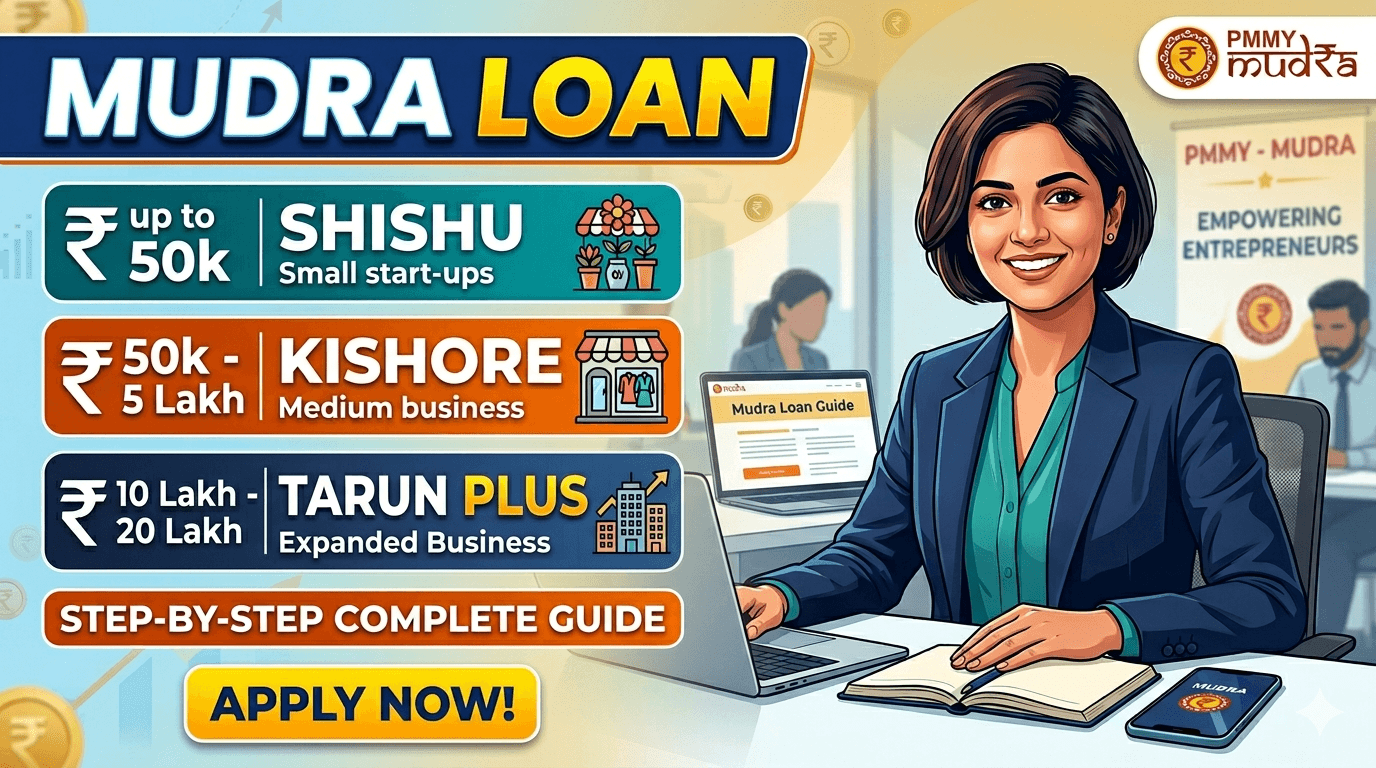

Shishu – For Brand New Businesses

Loan amount: Up to ₹50,000

Who can apply: Anyone with a business idea. You do not need previous business experience. You do not need a CIBIL score.

Papers needed: Only one page application form + identity proof (Aadhaar, PAN)

What happens if you use the money for personal needs: The bank will ask for all the money back immediately.

Easy explanation: Start here if you have never run a business before. Banks expect very few papers.

Kishore – For Small Growing Businesses

Loan amount: ₹50,001 to ₹5,00,000

Who can apply: Businesses that have been running for at least 6 to 12 months

Papers needed: Bank statement showing 6 months of business transactions

Easy explanation: You need to prove your business exists and earns money.

Tarun – For Established Businesses

Loan amount: ₹5,00,001 to ₹10,00,000

Who can apply: Businesses that have been running for 2+ years and pay taxes

Papers needed: Income tax returns for 2 years OR GST returns for 4 quarters

Easy explanation: The bank wants to see that you have a real, growing business.

Tarun Plus – New Category (2026)

Loan amount: ₹10,00,001 to ₹20,00,000

Very important rule: You must have already taken and fully repaid a Tarun loan before. You cannot apply for Tarun Plus directly.

Source: Government announcement (PIB Delhi, March 14, 2026)

Easy explanation: You cannot skip levels. First take Tarun, repay it fully, then ask for Tarun Plus.

Quick Reference Table

Mudra Tier Comparison Matrix

| Category Tier | Target Funding Limit | Required Business Vintage | Institutional CIBIL Check? |

|---|---|---|---|

| Shishu | Up to ₹50,000 | None (Startups/New ventures welcome) | No Minimum |

| Kishore | ₹50,001 to ₹5 Lakh | 6 to 12 Months actively operational | Sometimes |

| Tarun | ₹5,00,001 to ₹10 Lakh | 2+ Years established vintage | Yes (750+ Ideal) |

| Tarun Plus | ₹10,00,001 to ₹20 Lakh | Must have perfectly closed past Tarun limits | Strict Evaluation |

Enter your target asset funding requirements below to see your operational track record goals and credit evaluation flags.

Who Can Apply and Who Cannot

Businesses That Qualify (The Allowed List)

You can use Mudra loans only for non-farm businesses that earn money. Here are some examples:

- Making and selling products (papad, agarbatti, pickles, bakery items)

- Running a shop (kirana store, mobile recharge shop, garment stall)

- Services (tailoring, beauty parlor, mobile repair, computer training)

- Transport (e-rickshaw, goods carrier, taxi)

- Food business (catering, tiffin service, food stall)

Real example: A fruit seller in Mumbai took a ₹40,000 Shishu loan to buy a hand cart and stock. Within 8 months, his daily earnings went from ₹200 to ₹600.

Businesses That Do NOT Qualify (Automatic Rejection)

You cannot use Mudra loans for:

- Farming on agricultural land (use Kisan Credit Card instead)

- Selling alcohol or gambling

- Buying or building a house

- Paying back other loans

- Paying for college or coaching classes

Easy explanation: If your business is selling vegetables from a shop, you qualify. If your business is growing wheat on your farm, you do not qualify.

Can a Housewife with No Business Experience Apply?

Expert advice from Neha Gupta (financial trainer with 15+ years experience):

"A housewife with no prior business experience can apply for Shishu loans up to ₹50,000. However, she must present a credible business plan. Banks will ask: Where will you operate? How will you manage inventory? Without convincing answers, rejection follows. I have personally guided over 200 women entrepreneurs through this process."

Real example: Rekha, a homemaker in Bangalore, applied for a ₹40,000 Shishu loan to start a tiffin service. She had no prior business. The bank approved her because she showed:

- A registered kitchen address

- Three potential bulk orders from nearby offices

- Her husband as a co-signer

Within 8 months, she qualified for a larger Kishore loan.

Key lesson: Not having experience does not mean automatic rejection. Not having a clear plan does mean rejection.

Mudra Loan: Essential Documents Checklist

Important Note: This list is a general guide. While these are the standard requirements, your bank may request additional paperwork depending on your specific profile.

1. Common Identity & Address Proofs (For Everyone)

Har loan category ke liye yeh documents sabse pehle taiyar rakhein:

- Primary KYC: Aadhaar Card & PAN Card (Mandatory)

- Backup Identity Proof: Voter ID Card OR Passport

- Photographs: 2 recent passport-size photographs

2. Business Proof (Any One Document Required)

Apne business ki validation ke liye niche diye gaye documents mein se koi ek submit karein:

- Udyam Registration Certificate (Highly recommended – free to get online)

- Shop Establishment Certificate

- Trade License from your local municipality

- Gumasta License (Specifically required in Maharashtra and a few other states)

Extra Documents by Loan Category

1. 1. Shishu Category

- KYC Documents (Aadhaar, PAN, etc.)

- Business Proof (Any one proof; a one-page application is sufficient)

2. Kishore Category

(Shishu ke documents ke sath yeh bhi add karein):

- Bank Statement: Last 6 months ki business transactions ki statement.

- Business Address Proof: Rent agreement ya electricity bill.

3. Tarun & Tarun Plus Category

(Kishore ke documents ke sath yeh bhi add karein):

- Tax Proof: 2 saal ki Income Tax Returns (ITR) OR 4 quarters ki GST returns.

- Repayment Proof: Pichle Mudra loans ko time par repay karne ka proof (Sirf Tarun Plus ke liye).

The Name Mismatch Problem (Sabse Badi Galti)

Common Issue: Online log report karte hain ki, "Bank ne mere documents reject kar diye kyunki Aadhaar par mera naam husband ke surname ke sath tha, aur PAN card par father ke naam ke sath."

The Fix (Ise Kaise Thik Karein?):

Application submit karne se pehle check karein ki aapka naam Aadhaar, PAN, aur Bank Account teeno par bilkul same hona chahiye. Ek single letter ki galti se bhi loan reject ho jata hai.

- Real Example: Lucknow ke ek mobile repair shop owner, Suresh, ka loan do baar reject hua kyunki Aadhaar par "Suresh Kumar" aur PAN par "Suresh K." likha tha. Unhone online PAN update kiya, 4 din wait kiya, aur reapply karne ke 2 hafte mein unka Kishore loan approve ho gaya.

Quick Action Step:

Apna Aadhaar aur PAN card side-by-side rakhein aur letter-by-letter naam match karein. Agar koi mistake hai, toh apply karne se pehle use online update karwayein. Yeh 3 se 5 din lega, lekin aapko hafton ki rejection se bacha lega.

Interest Rates (Updated June 2026)

Why Rates Are Different for Different People

Unlike fixed government schemes, Mudra loans come from different banks. Each bank sets its own rate based on their costs and your credit profile.

Important note: The rates shown below are general ranges as of June 2026. Your final rate depends on your bank, your loan category, and your repayment history.

Interest Rate Table by Bank Type

| Bank Type | Interest Rate (Per Year) | Processing Fee |

|---|---|---|

| Government Banks SBI, BOB, PNB, etc. | 8.05% - 11.50% | ₹0 or ₹500 |

| Private Banks HDFC, ICICI, Axis, etc. | 11.00% - 16.00% | Up to 1% of loan |

| NBFCs IIFL, L&T Finance, etc. | 14.00% - 22.00% | 1% - 2% of loan |

| Fintech Apps FlexiLoans, Razorpay, etc. | 8.00% - 16.00% | Varies by platform |

NPA Warning – Important to Know

What is NPA? When a borrower stops paying back a loan, it becomes a "non-performing asset" or NPA for the bank.

Statistic: Tarun category loans have default rates of 6% to 9%. Shishu loans have very low default rates of only 1% to 2%. (Source: Financial Express, December 2025)

What this means for you: Banks check Tarun applications very carefully. If your CIBIL score is below 750 or your business financials are weak, you may be rejected or offered a smaller loan.

Expert advice from Chakrivardhan Kuppala (Executive Director, Prime Wealth Finserv):

"The higher default rate in Tarun (6-9%) reflects that growing a business is riskier than starting one. Entrepreneurs often borrow too much without a solid plan to repay. The solution isn't to avoid Tarun – it's to get business advice and make realistic cash flow projections before applying."

How to Apply Step by Step

What to Keep Ready Before You Start

Before filling any form, gather these items:

- Aadhaar and PAN (names matching exactly)

- 2 passport-size photos

- Business address proof (rent agreement or electricity bill)

- Bank account in your business name (or personal account for Shishu)

- Mobile number linked to Aadhaar (for OTP)

Online Application (New 2026 Method)

The government has connected Mudra loans to the Jan Samarth portal (www.jansamarth.in) starting March 2026.

Steps to apply online:

- Go to Jan Samarth portal and register using your Aadhaar

- Select "PMMY – Mudra Loan" from the list of schemes

- Fill the online application (takes about 15 minutes)

- Upload scanned copies of your KYC and business proof

- Choose your preferred bank branch

- Write down the Application Number you receive

- Track your application status online anytime

Offline Application (Going to the Bank Branch)

- Visit the bank branch where you already have a savings or current account

- Ask for Form-I (Mudra loan application) – for Shishu, this is just one page

- Submit physical copies of all your documents

- The bank will send someone to verify your business location (for loans above ₹2 lakh)

- You will get a sanction letter within 7 to 21 days (official timeline)

- Money is sent to your bank account within 3 to 5 days after sanction

What Happens During Field Verification

What users report online: "The bank officer came at 9 PM and asked for money."

The truth: Bank officers must visit during working hours only (10 AM to 5 PM, Monday to Friday). The officer will:

- Take two photos (your shop and you working inside)

- Check that your business really exists at that address

- Talk to two neighbors or customers as witnesses

- Look at your stock or inventory (for shops)

What to do if someone asks for a bribe: Note the officer's name and employee ID. Report to the bank's nodal officer or call the Banking Ombudsman at 14448 (toll free). This is against RBI rules.

Why Applications Get Rejected and How to Fix

Top 5 Rejection Reasons with Solutions

The "Bank Said Mudra Loan Is Closed" Lie

What people report on Reddit and Quora: Bank staff say "Mudra scheme has stopped" to avoid extra paperwork.

Fact: The government plans to keep Mudra loans until 2030-31. The scheme is very much active.

Statistic: Over ₹33.65 lakh crore has been given out through 52+ crore Mudra loan accounts. (Source: Financial Express, December 2025)

What to do: If a bank employee tells you the scheme is closed, ask for their name and say you will file a complaint with the Banking Ombudsman. They will change their response immediately.

Think about this: If the scheme were really closed, why did the government add Tarun Plus in October 2024 and connect it to Jan Samarth in March 2026? Do not believe false information from bank desks.

Real Success Story – From Small Loan to Big Business

Story of Gupta General Store (Delhi)

| Year | Loan Category | Amount | What They Did | Result |

|---|---|---|---|---|

| Year 1 (2023) | Shishu | ₹40,000 | Bought more stock | Monthly profit up by ₹8,000 |

| Year 3 (2025) | Kishore | ₹3,00,000 | Renovated the shop | Sales up by 40% |

| Year 5 (2026) | Tarun | ₹9,00,000 | Opened a second shop | Total revenue doubled |

| Year 7 (2027) Goal | Tarun Plus | ₹15,00,000 | Start franchise model | Plan to open third location |

Lesson: Mudra loans are like climbing stairs. You cannot jump from the ground to the top. Each on-time repayment unlocks the next higher loan amount.

Mudra Compared to Other Government Schemes

Sometimes another scheme might be better for you than Mudra. Here is a simple comparison:

| Scheme | Loan Amount | Interest Help | Collateral Needed | Best For |

|---|---|---|---|---|

| Mudra (PMMY) | Up to ₹20L | No subsidy | No | Any small business |

| Stand-Up India | ₹10L to ₹1Cr | No subsidy | No | SC/ST/Women business owners only |

| PMEGP | Up to ₹25L | 15% to 35% subsidy | No | Manufacturing businesses |

| CGTMSE | Up to ₹5Cr | No subsidy | No (guarantee covers bank) | Existing businesses needing bigger loans |

Note: Some bank documents still show Tarun limit as ₹10L. This may not include the new Tarun Plus extension. Always check with your lender directly.

Frequently Asked Questions (12 Common Questions)

Q1. Can I get a Mudra loan without a CIBIL score?

Yes, for Shishu loans up to ₹50,000. For Kishore and above, most banks check your credit score. Some NBFCs may approve Kishore with low CIBIL but will charge higher interest.

Q2. What is the maximum loan under Shishu?

₹50,000. Applications for more than this go to Kishore or get rejected. You cannot take two Shishu loans to get more money.

Q3. Can I pay back my Mudra loan early without penalty?

For Shishu and Kishore: Yes, RBI says no penalty for early payment. For Tarun: Check your loan papers. Some NBFCs charge 2% to 3% for early closure.

Q4. Is Udyam Registration required for Mudra loans?

Not for Shishu. Strongly suggested for Kishore and Tarun. Required for Tarun Plus. Registration is free and takes 10 minutes online.

Q5. How long does Mudra loan approval take?

Official timeline: Shishu (7 to 10 days), Kishore/Tarun (15 to 21 days). In reality with perfect documents: 2 to 4 weeks. If documents have errors: 6 to 8 weeks.

Q6. Which bank gives Mudra loans most easily?

Government banks (SBI, PNB, BOB) approve more applications but take longer (4 to 6 weeks). Private banks (HDFC, ICICI) are faster (2 to 3 weeks) but stricter about CIBIL scores (750+ needed for Tarun).

Q7. What happens if I stop paying my Mudra loan?

The bank reports to CIBIL and your credit score drops for 7+ years. Legal recovery starts. They may take your assets. Any co-signer or guarantor also becomes responsible.

Q8. Can two family members get separate Mudra loans?

Yes, if they run completely different businesses with separate bank accounts, separate shop addresses, and separate income proofs. Husband and wife cannot get two loans for the same shop.

Q9. Is GST registration required for Mudra?

Only if your yearly turnover is above ₹40 lakh (for services) or ₹1.5 crore (for goods). For Tarun Plus, having GST registration is strongly recommended even if not required.

Q10. Does the government give interest subsidies on Mudra?

No direct subsidy from central government. But some state governments (UP, Tamil Nadu, Maharashtra, Karnataka) offer extra subsidies through their own schemes. Check with your local district industries office.

Q11. Can a minor (under 18) apply for a Mudra loan?

No. You must be at least 18 years old. For businesses run by minors, a parent or legal guardian must apply as the main borrower.

Q12. What is the difference between MUDRA and my bank?

MUDRA (the agency) does not give you money directly. It gives money to banks so they can lend to you. Your bank is the lender. You repay your bank, not MUDRA.

Final Checklist Before You Apply

Use this checklist to make sure you are ready:

- [ ] Pick the correct loan category based on your business stage (do not ask for more than you need)

- [ ] Check that your Aadhaar and PAN names match exactly

- [ ] Register on Udyam portal (free, 10 minutes) – not required but helps approval

- [ ] Write a simple one-page business plan (needed for Kishore and above)

- [ ] Keep 6 months of bank statements ready (needed for Kishore and above)

- [ ] Apply through Jan Samarth portal (www.jansamarth.in) for easy tracking

- [ ] Save your application number immediately after applying

- [ ] Never pay any "agent" or "broker" – Mudra has no middlemen

Legal Warning: Lying about your business to get a Mudra loan (for example, saying you will run a shop but using the money for personal needs) is fraud under Indian law. Banks can take back the loan immediately and start criminal proceedings.

If your application is rejected even after you meet all requirements, complain to the Banking Ombudsman at 14448 (toll free). Do not give up on your legal right.

2 thoughts on “Mudra Loan Complete Guide: Shishu, Kishore, Tarun”